Large Contracts (HSI) vs Mini Contracts (MHI) Core Differences Overview

[Contract Value Comparison] How Much Do You Gain or Lose per Point Movement?

The core difference between large and mini contracts lies in the “contract multiplier”, which determines how much your account increases or decreases for each point movement in the index.

- Large contracts (HSI): Each point is worth HK$50.

- Mini contracts (MHI): Each point is worth HK$10.

In other words, the contract value of mini contracts is one-fifth of large contracts. For example, if the Hang Seng Index rises from 18,000 to 18,100, an increase of 100 points:

- If you go long one large contract, the profit is: 100 points * HK$50/point = HK$5,000.

- If you go long one mini contract, the profit is: 100 points * HK$10/point = HK$1,000.

The calculation for losses is the same. The profit and loss fluctuations of mini contracts are significantly smaller than those of large contracts, making them more suitable for beginners with limited capital or lower risk tolerance.

[Margin Differences Between Large and Mini Contracts] Initial Margin vs Maintenance Margin Explained

Margin, commonly referred to as “deposit”, is the most important concept in futures trading. It is not a trading cost, but a sum held in your broker account to ensure you can fulfill contractual obligations. Margin is divided into two types:

- Initial margin: Also known as “basic margin”, this is the minimum amount of funds required in your account when opening a new futures position (whether long or short).

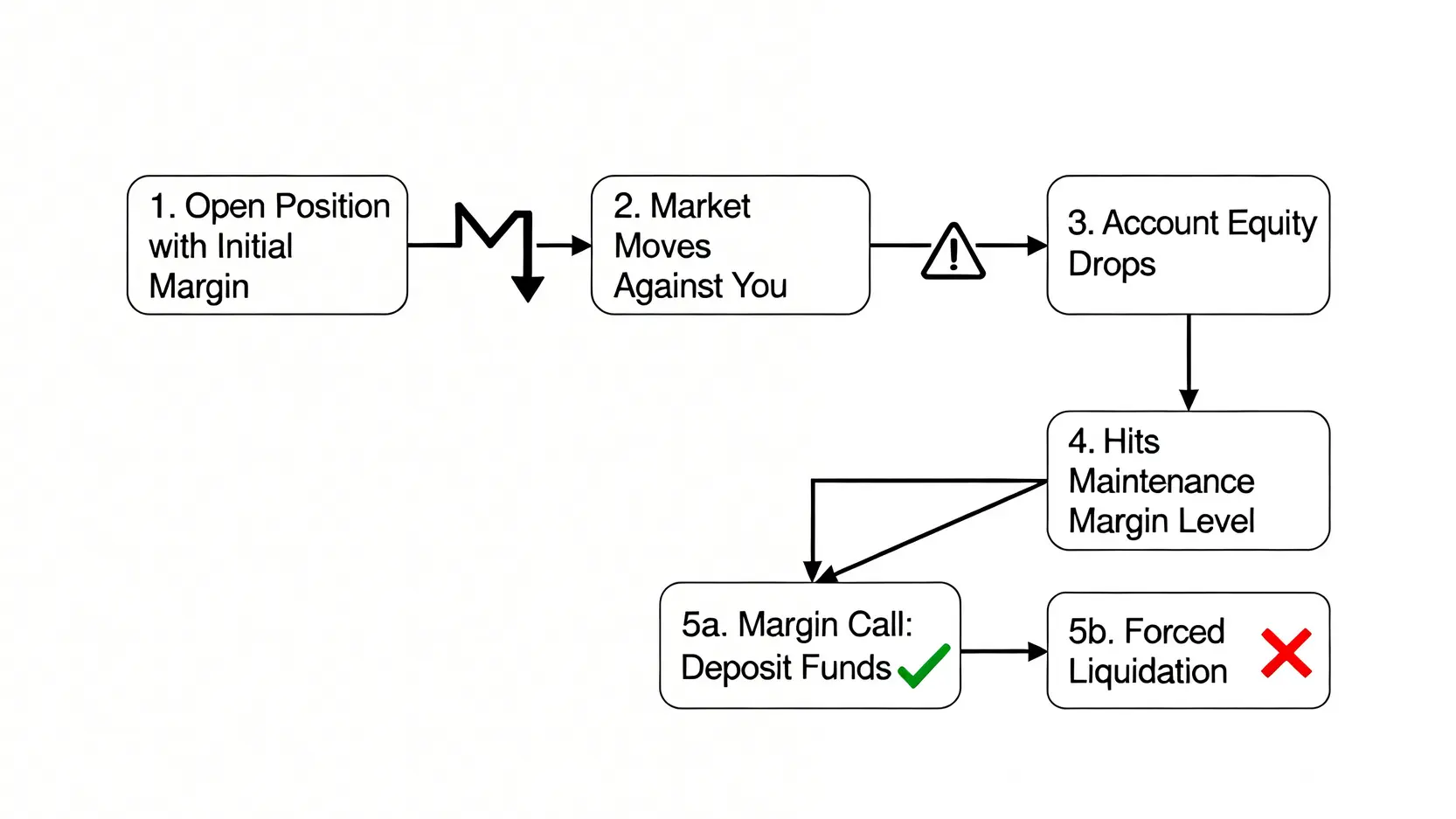

- Maintenance margin: After you hold a position, if market movements turn unfavorable and your margin level falls to this threshold, the broker will issue a “margin call”, requiring you to deposit additional funds to restore it to the initial margin level, otherwise forced liquidation will occur.

Since large contracts have a higher contract value and greater risk, their margin requirements are significantly higher than those of mini contracts. The following is a reference example (please note that margin amounts may be adjusted by the Hong Kong Exchanges and Clearing Limited based on market conditions. Always check the latest requirements before trading):

| Contract Type |

Initial Margin (Reference) |

Maintenance Margin (Reference) |

| Large Contracts (HSI) |

~ HK$80,000 – HK$120,000 |

~ HK$64,000 – HK$96,000 |

| Mini Contracts (MHI) |

~ HK$16,000 – HK$24,000 |

~ HK$12,800 – HK$19,200

|

[Mini Hang Seng Entry Cost Calculation] Trading Cost Comparison, How Should Beginners Choose?

The true “Mini Hang Seng entry cost” does not refer to margin alone. A complete trading cost should also include broker commissions and other miscellaneous fees. A more prudent capital preparation strategy is:

Actual entry cost = initial margin + trading costs (round-trip commissions, exchange fees, etc.) + additional buffer funds

It is strongly recommended to prepare at least an additional 30-50% of funds beyond the margin as a buffer to cope with market fluctuations, avoiding being forced to add margin or undergo forced liquidation due to minor losses. For example, if the initial margin for Mini Hang Seng is HK$20,000, a relatively safe starting capital would be HK$26,000 – HK$30,000.

Beginner selection advice:

Without a doubt, for beginners or investors with smaller capital, starting with “Mini contracts” (Mini Hang Seng Index futures) is the only reasonable choice. It has a lower threshold and relatively controllable risk, allowing you to learn how the market operates and test your trading strategies at a lower cost. Once you have accumulated sufficient experience and capital, you can then consider switching to large contracts.

Understanding “Hang Seng Index Futures Leverage”: A Wealth Amplifier or a Risk Beast?

Leverage is the most fascinating and most dangerous feature of futures trading. It allows you to “do ten units of work with one unit of capital”, but losses will also erode your principal at the same multiple. Understanding how Hang Seng Index futures leverage works is the first step in risk management.

Leverage Principle: How to Control Large Contracts With Small Capital?

The formula for calculating leverage is very simple:

Leverage ratio = total contract value / initial margin

Where total contract value = current index level * contract multiplier.

Assume the Hang Seng Index is at 18,000 points, and the initial margins for large and mini contracts are HK$100,000 and HK$20,000 respectively:

- Large contract value = 18,000 * HK$50 = HK$900,000

Large contract leverage ≈ HK$900,000 / HK$100,000 = 9 times

- Mini contract value = 18,000 * HK$10 = HK$180,000

Mini contract leverage ≈ HK$180,000 / HK$20,000 = 9 times

From the calculation, it can be seen that under official margin requirements, the leverage ratios of large and mini contracts are theoretically similar. This means that every 1 unit of margin you invest actually controls assets worth 9 units. Your return rate and loss rate will both be amplified 9 times.

Leverage Risk Calculation and Margin Call Mechanism

The core of leverage risk lies in “forced liquidation”. When your losses erode your margin below the “maintenance margin” level, a Margin Call will be triggered.